Here is one of the first platforms I ever wrote about, so I have followed it closely for the past 1.5 years. Here’s my view into what happened.

Building Here

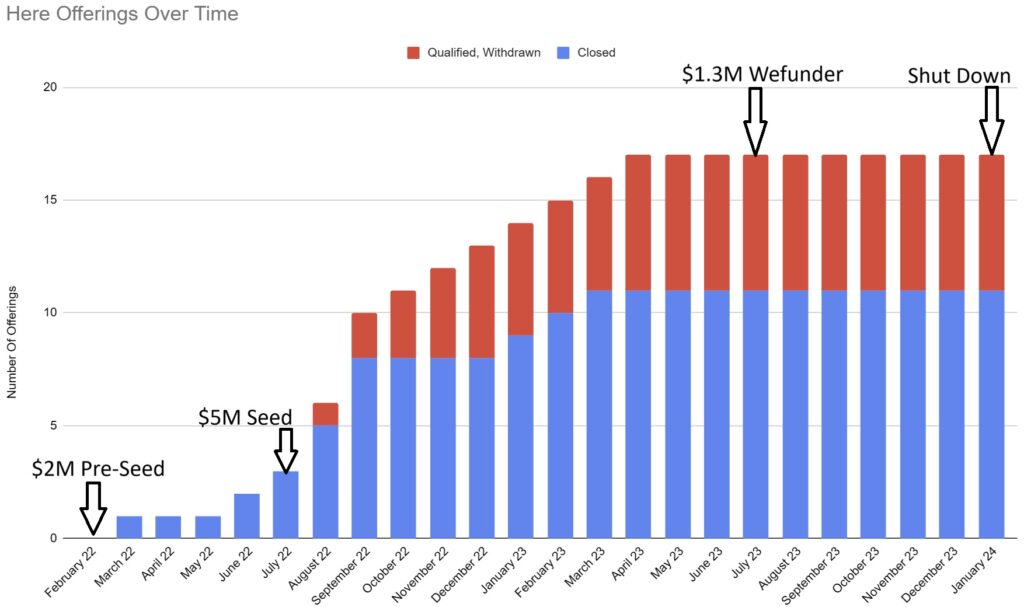

- Here Investments Inc. incorporated on February 22, 2021.

- One year later, in February of 2022 they received $2M in pre-seed funding.

- Shortly after, they closed their first offering that March.

- They would go on to close 2 more offerings by July of 2022. The third offering sold out in only about 30 minutes.

- This was apparently a good backdrop for fundraising, as they landed $5M in seed funding.

- This clearly put gasoline on the fire. After closing only 3 offerings in their first 18 months, they closed 5 in the next two months.

- They would close a total of 11 offerings before raising $1.3M on Wefunder in July of 2023.

- Unfortunately, there weren’t any positive updates before the announcement they were shutting down on January 4, 2024.

Problems With Here’s Real Estate Platform

Let’s take a deeper dive into the problems that I think lead to their failure. We’ll focus on 4 different areas in detail.

1. Low Offering Success Rate

One of the first signs of growing pains comes from the red in the graph above. Those are offerings that were sourced, successfully qualified by the SEC, but withdrawn.

In several cases these were either advertised publicly or were available for preview on the site. In at least one case investors had contributed funds before the offering was withdrawn (refunds were later issued).

In the end, Here only successfully launched 11 of their 17 qualified offerings. That amounts to about a 65% success rate.

The reasons for offerings being withdrawn were varied. In many cases, no reason was given. Other cases were simply due to an apparent lack of traction / investor interest. At least one time financing and interest rates were the culprit:

Due to rapid changes to the US interest rate environment, we have decided to terminate the Magnolia offering, as it does not appear that we will be able to close this purchase with favorable debt terms.

As a result, all Magnolia investments will be canceled…

Here’s Investor Relations Team

These are of course only the properties that made it to SEC qualifications. We have no idea how much time and capital were spent evaluating ones that didn’t even make it that far.

Even then, having to throw away 35% of their efforts without returning any revenue for the investment had to hurt, especially for an unprofitable company.

Additionally, the company surely faced costs to set up the fractional offerings and to secure the properties.

2. Unique No More

Another factor we should touch on was the fleeting novelty of the platform. When Here launched the first fractional vacation rental property, to my knowledge, they were the first to market with this type of offering for non-accredited investors.

That uniqueness only lasted so long though. In September of 2022, Arrived Homes entered the game. Within a few days of launching, Arrived already had 7 vacation rental offerings. At that time, Here had 10 qualified offerings with only 8 closing successfully.

In many ways, this was simply just not a fair fight. Arrived has raised a staggering $162M in funding, or approximately 80 times the amount Here raised.

Lofty, Ark7, and Fundhomes have now also had at least one vacation rental offering. So, what was once a unique investment product simply became one of many options.

3. A Tenuous Business Model

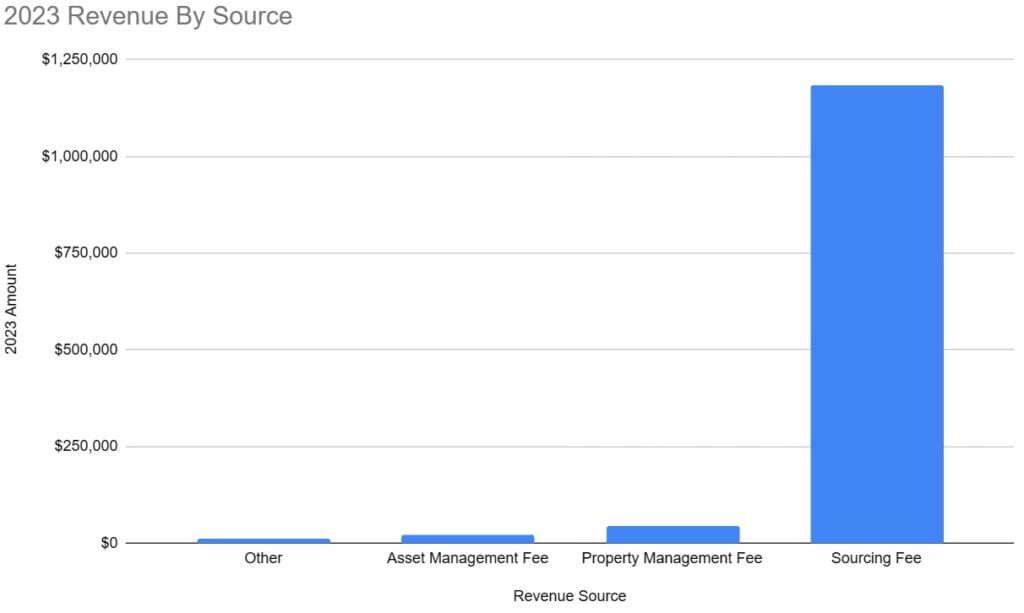

Here aimed to make money through 3 different types of fees:

- Asset Management Fee – 0.25% of the “asset value” each quarter

- Property Management Fee – 25% – 40% of property gross receipts

- Sourcing Fee – 10-20% of the purchase price + 10-20% of repair/furnishing costs

You might imagine that a fleet of highly productive vacation rentals would generate revenue from the Asset and Property Management fees. However, based on Here’s Form C, that’s not the case at all.

About 94% of their revenue came from the sourcing fee. Property Management was ~3.5%, Asset Management was ~1.6%, and “Other” was ~1.1% of total revenue.

The asset management fee is unsurprisingly low. The opportunities for growth are mainly through the appreciation of the properties, which requires time and good fortune. I can’t speak for what the other revenue was, but let’s just assume that’s within expectations.

That leaves two which are worth a deeper discussion.

Property Management Fee – Execution Issues

The revenue from this is actually shockingly low.

The vast majority of Here properties charged 25% for this. If we use that for calculations, we can roughly guess the total revenue from 11 offerings and over $10M in real estate was… $174K.

That calculates out to an approximate 1.7% gross yield.

That is, of course, somewhat unfair since not all properties were bookable for all of 2023 and the lag time from bookings going live to bookings actually occurring.

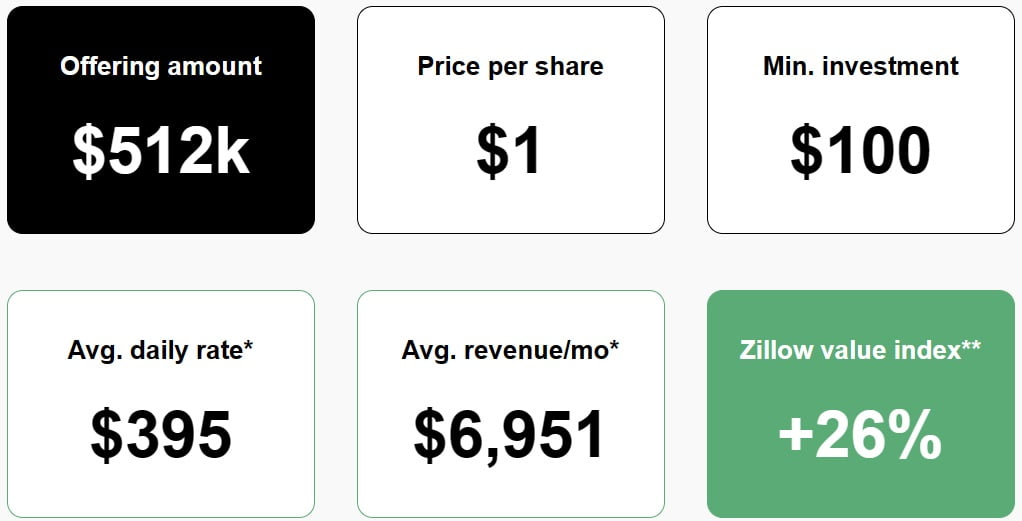

Even allowing some wiggle room for that, this result is simply abysmal. To put it in context, this is what expectations looked like for one property:

This is from “Mendocino” in Galveston, Texas. The average monthly revenue is based on data from AirDNA for the 75th percentile of 3-bedroom rentals in 2022 in the area. This average monthly revenue would translate to $83,412 per year. That’s 48% of the $174K Here generated for 11 properties in 2023.

Since this property was active in Q4 ‘22 (based on investor payouts and emails from the company), it seems safe to assume it was active throughout ‘23 as well. That means it didn’t perform anywhere near the AirDNA benchmark.

There are two simple potential explanations. Either the market was significantly worse in 2023, or Here didn’t live up to the 75th percentile. In June of ‘23, AirDNA updated their full year forecast for 2023. Things were only expected to be slightly different than the year prior, -1.1% RevPAR. In other words, after 5 months of data, AirDNA expected 2023 to be about the same as 2022 – no signs of a total market crash anywhere.

It simply seems that Here was not able to reach performance that was even close to the 75th percentile. It doesn’t seem like they were even average.

Aside from disappointed investors, this has a critical business impact. Since Here decided to do property management in-house, they also have staffing expenses for it.

The $43,487 in property management fees they received is equivalent to $21/hour for 40 hours a week for an entire year. Even if they only had one full time employee to manage all 11 properties, it’s likely they had to pay more in salary than they received in fees.

Sourcing Fee – Overreliance

This was 94% of revenue for the company. This has two major complications. First, it means the company needs to close offerings in order to really make money. The faster and more efficiently they could do that, the easier it would have been to scale and reach profitability.

However, as we previously documented, this was not something that Here was good at. Other than a brief period after their seed round, the company struggled to get offerings onto and sold through the platform.

The second major issue is that it provides poor incentives for the company. Rather than bringing quality offerings, in order to survive, what they really needed to do was get anything they could sell onto the platform as quickly and efficiently as possible.

We’ll ultimately never know, but you have to wonder how many offerings were just put up in an effort to generate revenue for the next funding round.

Conclusion – Outgunned & Outmaneuvered

Here’s revenue shows several flaws with the company’s strategy. A low interest rate environment, a boom in almost all asset classes, and a lack of competitors may have initially given the company some life. But all three of those pillars came under assault, exposing the weaknesses within.

In the end, Here was outgunned and outmaneuvered. Arrived wasn’t first, but they were very savvy with their entrance into the space.

Starting with a property manager partner kept them from having to onboard property managers. It also let them hand-pick companies that had experience in a particular market. They then used this light-weight structure to scale easily – bringing multiple properties in the same market with the same partners.

The vacation rental properties from Arrived also have lower fees, something that would have eventually put pressure and longevity on the financials of Here’s offerings.

Then put the cherry on top that Arrived had 80X more funding and Here was always going to be in a challenging competitive position, even with great execution.

4. Poor Expense Management

In an environment where many companies made difficult decisions around staffing and strategy to preserve capital, Here did the opposite.

From 2022 to 2023, here’s the increases in expenses, per category:

- General & Administrative Expenses – 85.57% YoY increase

- Marketing & Advertising Expense – 888.14% YoY increase

- Other Expenses – 1372.67% YoY increase

- Payroll & Related Expenses – 890.69 YoY increase

- Professional Services – 322.52% YoY increase

In fact, the marking and advertising costs were 62% of total revenue. Does that mean they had to constantly spend money to acquire new users to move shares of their 3 offerings that year? They might have had more success just cutting fees by 50%.

What About The Wefunder Funds?

Before we wrap up, we should talk a bit about the Wefunder raise. They were able to pull in $1.3M relatively recently. The fact that the company is shutting down 6 months later seems to have shocked many investors in the company.

We’ve covered issues with their business model. There are plenty of them. In 2023, that netted to a loss of $2.3M. That means they were burning through over $191K/month with revenue from 3 successful offerings.

At that rate, $1.3M would last somewhere between 6 and 7 months. I’m sure they took measures to extend their runway, but that could easily have been offset by the lack of revenue from new offerings.

I also suspect there was considerable time spent on things like pivoting the business, pursuing acquisitions, and attempting further fundraising. Even the decision to shut down may have come after various legal consultations. None of that would have been free.

Conclusion – The End Of Here

After a myriad of failures, Here has shut down. The properties will be disposed of quickly, almost assuredly at losses for investors. It will be very difficult to recoup the full purchase price of the property, plus the 10-20% sourcing fee, plus closing costs on both sides, plus any exhausted cash reserves.

Unfortunately, I think investors recovering even 50% of the original offering is likely a decent outcome in this context.

Anyone that is still interested in fractional investing for vacation rental properties should check out Arrived Homes. While they also haven’t had any recent offerings in this space, Arrived is in many ways a superior, lower-fee version of what Here was putting in front of investors.

Originally sent to newsletter subscribers on January 22nd.